Image: Marriner S. Eccles Federal Reserve Board Building. Source: traveler1116 / iStockphoto

Stock index futures are nominally higher ahead of the market open, with S&P 500 futures 0.2% higher, Nasdaq 100 futures up 0.3% and Dow 30 futures 0.1% better as of 8:30 am EDT.

Last week, the major indexes all posted modest gains by Friday, after a week that saw two-way trading amid lighter-than-usual volume. The S&P 500 inched 0.1% higher, the Nasdaq Composite added 0.7% and Dow Industrials gained 2.75%.

All eyes remain squarely on the Federal Reserve, with the number and magnitude of interest rate hikes this year still a question of debate. Friday’s jobs reports showing growth in non-farm payrolls of 431,000 in March may have alleviated some concerns about an economic slowdown, but there remain reasons for concern.

Inflation remains top of mind, both for the Fed and for consumers, as prices are rising at their highest rate in 40 years. This Wednesday’s release of the Fed’s minutes from the last meeting may offer some clues.

The bond market is also signaling that the Fed could act even more aggressively than anticipated, as US Treasury yields are inverted this morning for a third straight day.

On Thursday, the yield on the 2-year note rose above that of the 10-year note for the first time in two years. This inversion continued Friday and has occurred again Monday morning. The 2-year is yielding 2.41%, while the 10-year is at 2.38% as of 8:30am ET.

Since 1969, each of the last eight recessions has been preceded by an inversion of the yield curve. We’d caution that the current inversion may be different, however, given the Fed’s extraordinarily large balance sheet and a very low global interest rate picture.

The ongoing battle in Ukraine also continues to weigh on markets, as the latest evidence of Russian war crimes will undoubtedly lead to further sanctions by the US and Europe this week.

Key reports on our radar this week:

Monday: Factory orders

Tuesday: Services PMI; earnings from Acuity Brands (AYI), Novagold (NG)

Wednesday: Fed minutes; earnings from Exelon (EXC); RPM (RPM), Levi Strauss (LEVI)

Thursday: Jobless claims; earnings from Constellation (STZ); ConAgra (CAG), Lamb Weston (LW)

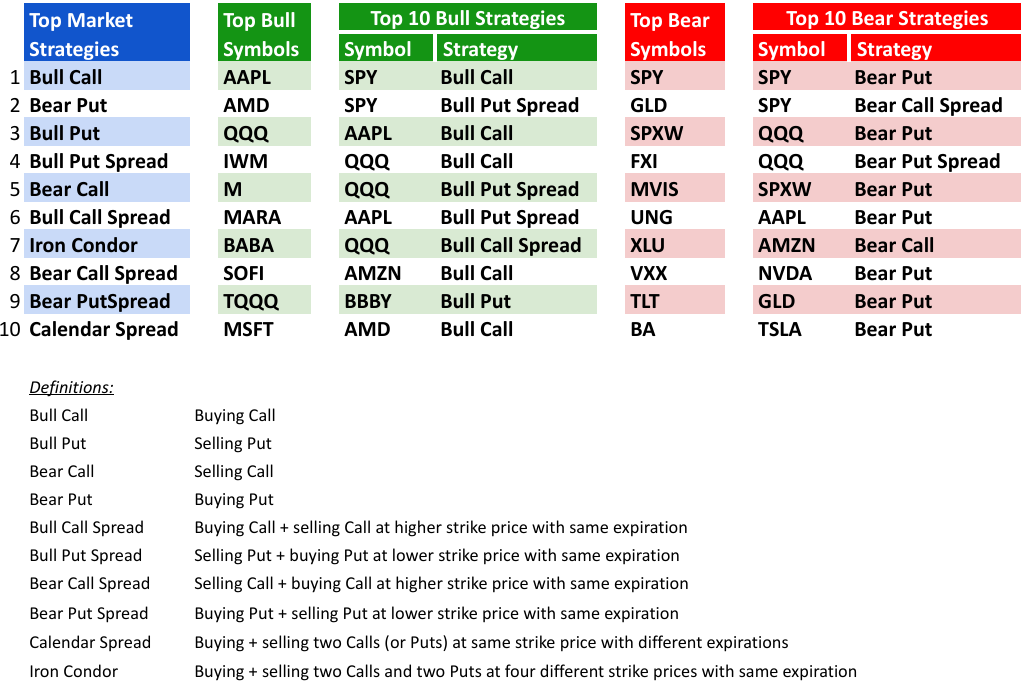

In examining options market data provided by Tradier API, we saw significant bull interest in Apple (AAPL) and AMD (AMD). Apple shares consolidated a bit last week after hitting a nearly three-month high on Tuesday. AMD shares also peaked on Tuesday after a sharp two-week rally, after which it gave back 12% the rest of the week.

Among bear names, most of the activity was centered on ETFs, but there was interest in MicroVision (MVIS) and Boeing (BA) options. MicroVision is the latest darling of the Reddit boards, and investors overreacted to a modest patent announcement made last Tuesday that sent the stock up 30%. MVIS gave back most of that gain over the next three trading sessions.

Boeing shares hit a ceiling last week after a three-week rally that saw the stock gain over 15%. The investigation over the crash of the 737 aircraft in China two weeks ago may cast a shadow for months to come.

Finally, we find it notable that the iron condor strategy attracted higher than usual interest from traders last week. The iron condor is most profitable in a sideways market with low volatility.

_____

Source: Equities News